Buy Now Pay Later – what are the pitfalls?

How far should governments go to protect people against their own self destructive instincts?

There are times as a financial researcher when you get to look into the belly of the money lending beast and you recognise that not every product is being used in the way the product information material intended.

The introduction of Buy Now Pay Later (BNPL) products (such as Afterpay and ZipPay) into the Australian marketplace has significantly changed consumers’ perceptions of credit.

Around a quarter of Australian adults have used BNPL, with the products particularly popular among Gen-Y and Z consumers (aged between 18 and 35). Indeed, a large part of Afterpay’s value proposition for businesses is ‘access’ to Gen Z and millennial consumers. Frictionless processes and slick apps characterise the product – it takes less than a minute for users to sign up to around $600 of credit with Afterpay. Platforms also spruik their merits as helping consumers’ ‘smooth consumption’ by spreading out a lump sum payment into three fortnightly chunks, with no interest charges – only late payment and possibly ‘account administration’ fees. Indeed, the value proposition for savvy consumers is quite clear – you are too intelligent to be paying interest.

The eyes wide shut loan scheme

However, BNPL has come under increasing scrutiny, in part because of the limited affordability checks that are undertaken by some platforms. Unlike credit cards, BNPL platforms operate largely outside the conventional bureau system, which is used be financial service providers to keep track of consumer loan applications and repayments. Platforms do not consult external bureaus to see whether consumers are experiencing difficulties in making their repayments, nor do they provide transparent reports about the repayment behaviour of their customers.

The seeming lack of due diligence does not necessarily mean that BNPL is bad for consumers, but it does make it difficult to address areas of potential concern. The Good Shepherd and other financial counsellors argue that BNPL contributes to the exploitation of vulnerable consumers. Women in coercive relationships, for example, have had accounts opened in their name. Another counselling agency, The Way Forward, found that 80% of their clients had used BNPL – and that BNPL users were less concerned than non-users about making themselves more financially vulnerable.

Who are BNPL’s people?

Together with the Commonwealth Bank of Australia, I have undertaken research to gain a further understanding of the BNPL user base. In the opaque information environment in which BNPL lies, it has been difficult to determine exactly how many of the millions of Australians who use BNPL hold accounts with more than one provider. Accessing credit outside the conventional bureau system creates an increased level of information asymmetry – without a clear picture of a borrower’s situation, lenders may assume that consumers already have BNPL accounts and ration accordingly. In other words, even if you don’t use BNPL, lenders may need to assume that you do to limit their own risks.

More importantly, our research seeks to uncover whether consumers who hold multiple BNPL accounts represent a riskier portion of the population. While it may seem like a sensible option for people to take advantage of offers such as ‘Afterpay Day’ or other platform-specific incentives, it is more likely to be driven by a shortage of liquid funds on the part of the consumer.

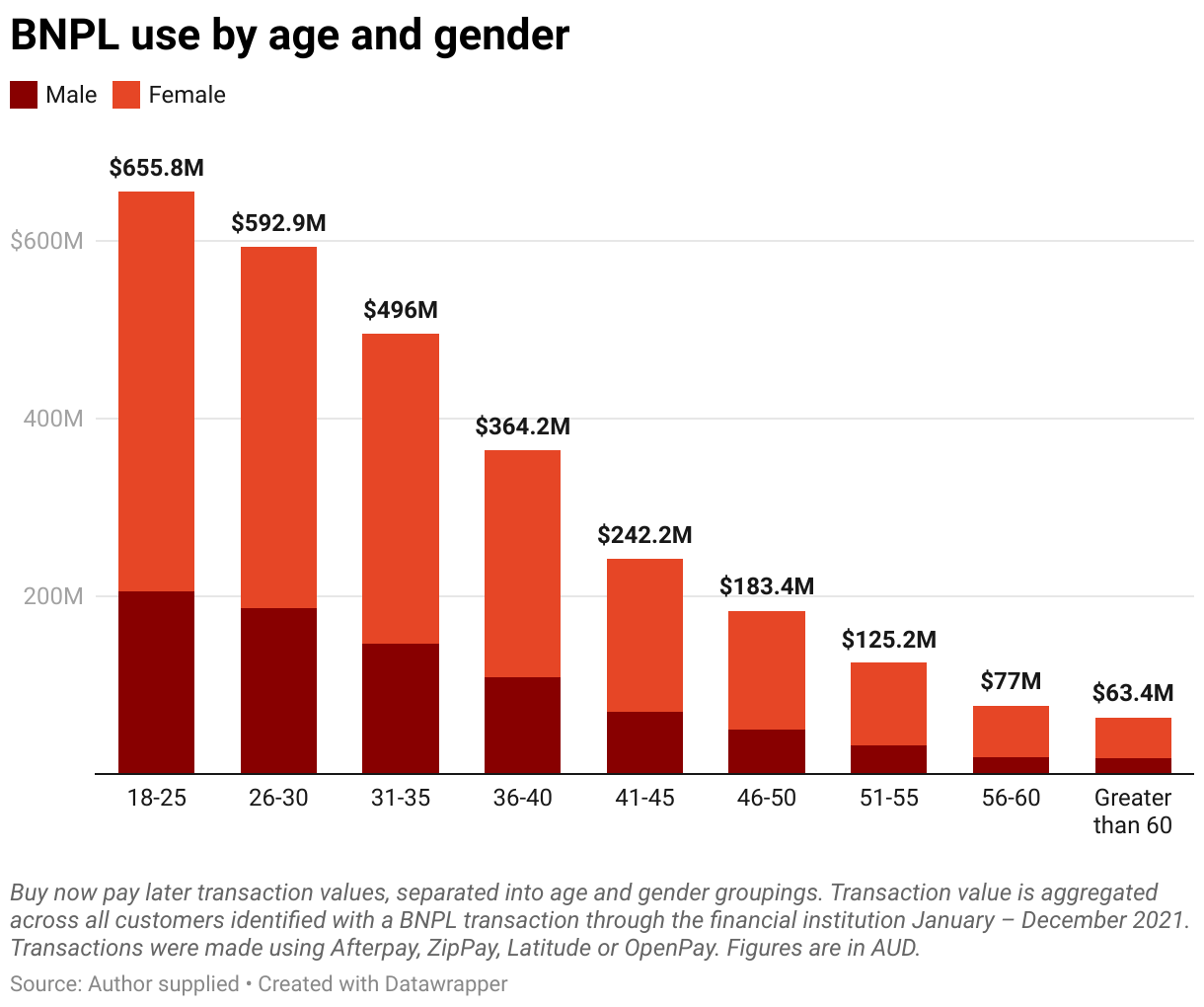

Our research finds that BNPL users are disproportionately from lower socioeconomic postcodes, while skewing heavily female (almost two-thirds of BNPL volume was from women) and towards younger consumers. The demographic patterns are aligned with both the marketing of BNPL and potential liquidity demands for people with casual employment.

Around 40% of consumers with BNPL accounts use more than one provider, meaning there is significant overlap between the user bases claimed by the platforms (it is not an ‘either/or’, but rather a ‘both’ decision). Moreover, consumers with multiple accounts spend nearly twice the amount on BNPL than consumers with only a single account. Rather than using BNPL funds for selective purposes (e.g., to catch a particular bargain) consumers appear to be using them as an ‘easy’ source of ready cash, often to fund essential purchases.

Our research revealed that around 30% of BNPL users also hold a credit card. This raises concerns about ‘debt-stacking,’ where consumers pay off interest-free debt (BNPL) with interest-incurring debt (credit cards). This has the potential to lead consumers to spiral out of control, as payments grow larger over time. One key motivator for taking out BNPL is having a maxed-out credit card. Consumers in search of funds, particularly those who are unable to obtain a credit limit increase, appear to turn to BNPL to top up their balance. Down the track, consumers with BNPL are more likely to view their credit card as disposable, leading to higher rates of delinquency and default.

BNPL encouraging younger consumers into a life of debt

The first foray into credit for many younger consumers has been through BNPL. There are broad similarities between BNPL and a credit card – payments in instalments over time, limited spending capacity – and the product is viewed as a starting point before ‘graduating’ to a real credit product. However, while BNPL providers do not report to credit bureaus, such consumers are missing out on the opportunity to build a credit record, which would allow them to benefit from on-time payments. Building a strong credit history allows consumers to benefit from access to lower-cost funds for future finance needs. Credit scores help consumers develop discipline with their repayments. An understanding that defaulting on loan repayments has ongoing consequences helps instil some level of self-control.

In May 2023, the Federal Government announced that regulatory changes were to be implemented, bringing BNPL into line with other consumer finance products such as credit cards and personal loans. The precise form of regulation has yet to be determined, but it will likely involve credit and affordability checks for consumers, as well as the provision of financial hardship plans. Undoubtedly, increased regulations will deter some consumers from using the products (either through increased frictions when using the product, or a preference to avoid regulated finance).

The tightening of regulation around BNPL should help protect vulnerable consumers from falling further into a financial hole. The alluring prospect of easily accessible BNPL funds has probably delayed consumers from seeking financial help at an earlier point in time, and the regulations are aimed at reducing financial harm. For the majority of users of BNPL, who are able to use the product successfully, striking the right balance between convenience and sensible safeguards will be important. Even with a higher cost of regulatory compliance, including reporting to credit bureaus, BNPL platforms will benefit from lower delinquency rates and a more sustainable model.

Dr Grant recently co-authored a paper on BNPL customer activity:

Boshoff, E., Grafton, D., Grant, A.R. and Watkins, J., ‘Buy Now Pay Later: Multiple Accounts and the Credit System in Australia’ (October 15, 2022). http://dx.doi.org/10.2139/ssrn.4216008

Image: Ma Fushun

Andrew is a Senior Lecturer in the Discipline of Finance at the University of Sydney Business School. His research covers a wide range of topics, mainly based around individual behaviour in financial and betting markets.